By pittsburgh-merchantservices October 17, 2025

Launching and growing a company in the United States means getting paid quickly, securely, and at a price point that won’t eat your margins.

The good news: affordable payment solutions for startups and small businesses now span card-present, online, mobile, invoicing, and real-time options—each with tools to cut costs, speed up cash flow, and reduce risk.

This guide translates the alphabet soup (ACH, RTP, PCI DSS, 1099-K, MFA, P2PE) into clear steps you can apply today. You’ll learn how to select processors, compare pricing models, minimize fees, accept modern tenders (wallets, pay-by-bank, instant), stay compliant, and build a payment stack that scales without surprises.

Throughout, we keep the focus tight: practical, U.S.-specific moves that lower total cost of acceptance while keeping checkout conversion and cash flow high.

How to Choose an Affordable Payment Stack That Scales (Without Overpaying)

When you’re short on time and budget, it’s tempting to click the first “easy” payment button. Resist. The most affordable payment solutions for startups and small businesses balance five forces: (1) acceptance coverage, (2) conversion, (3) operating cost, (4) cash-flow timing, and (5) risk & compliance.

Start by mapping where and how customers will pay: in-person (countertop, mobile), online (checkout, subscriptions), invoices (B2B, field services), and instant (RTP/FedNow, payouts). Then shortlist providers that support all target channels on one contract, so you avoid duplicate monthly fees, duplicate PCI scope, and data silos.

Press for transparent pricing in writing. Flat-rate aggregators are convenient but can hide overages (add-on fees for keyed entries, chargebacks, cross-border, or currency conversion). Interchange-plus is typically more affordable at scale because you see actual card network costs plus a fixed markup.

Prioritize providers that allow pay-by-bank (ACH, Same Day ACH) for invoice and subscription flows, because your blended acceptance cost can drop substantially when you steer eligible customers to lower-cost rails.

Finally, think data portability—tokenized cards on file should be yours to take if you ever migrate, ensuring leverage in future pricing talks.

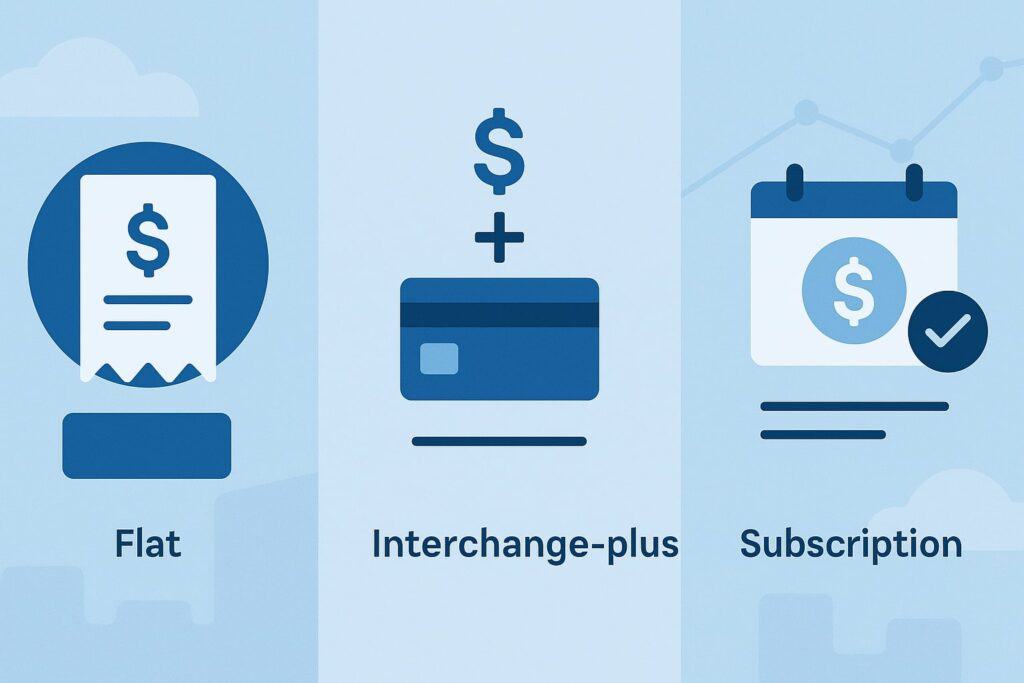

Pricing Models Explained: Flat, Interchange-Plus, and Subscription

Pricing drives total cost more than almost any other factor, making it central to affordable payment solutions for startups and small businesses. Three common models:

Flat rate (e.g., 2.9% + $0.30): ultra-simple, ideal for early MVPs or low volume. Downsides: you pay the same whether a transaction’s true interchange is cheap (debit, regulated debit) or expensive (rewards, keyed). As volume grows, flat rate becomes comparatively pricey.

Interchange-plus (e.g., Interchange + 0.20% + $0.10): transparent and usually more affordable at scale. You pay the actual network cost per transaction plus a fixed markup. Variance in interchange flows through, so strong debit mix or card-present EMV can materially reduce your effective rate.

Subscription/wholesale (e.g., $X monthly + small per-txn fee): a good fit when your monthly volume is predictable and sizable. You pay close to wholesale processing plus a fixed membership fee. Savings can be meaningful, but read the fine print on support, PCI fees, chargeback fees, and gateway fees.

Across all models, ask for card-present debit optimization, AVS/ZIP pass-through (for lower CNP interchange), and Level 2/Level 3 data for B2B cards (lowering interchange). Confirm whether PCI, gateway, and statement fees are included, waived, or negotiable.

The cheapest headline rate can still be more expensive once surcharges, batch fees, or monthly minimums are added.

Card-Present Acceptance: EMV, Tap-to-Pay, and Mobile Readers

For retail, pop-ups, food trucks, and services, in-person acceptance remains the conversion king. An affordable payment solution for startups and small businesses should support EMV chip, NFC contactless (Apple Pay/Google Pay), and tap-to-phone on recent smartphones—removing the need for separate hardware in some cases.

Key cost levers: hardware acquisition (buy vs. lease), device management (warranties, replacements), and network certification (firmware kept current).

Look for offline mode (where allowed), tips on glass, and QR fallback to complete sales even when connectivity dips. If you run multi-lane or multi-location, centralize device updates and settlement.

Negotiate no long-term terminal leases—they often inflate total cost. Pair in-person with a unified gateway so customer profiles and tokens work across channels, unlocking omnichannel features (buy online/pick up in store, in-app returns, loyalty). Security is non-negotiable: P2PE-validated solutions and tokenization reduce PCI scope and risk of data exfiltration.

As of March 31, 2025, new PCI DSS v4.x requirements became fully effective, making disciplined controls (like multi-factor auth for admins, stronger password policies, customized approaches monitoring) table stakes. If you’re upgrading terminals or platforms, confirm v4.x readiness during procurement.

Online Checkout and Subscriptions: Conversions Without Cost Creep

Ecommerce and SaaS demand a checkout that’s fast and flexible. To keep things affordable, tune for both authorization uplift and cost control. Offer major networks, wallets (Apple Pay, Google Pay, PayPal), and pay-by-bank for invoices and recurring charges.

Wallets reduce friction on mobile; pay-by-bank trims fees on high-ticket or repeat payments. Use network tokenization and account updater to reduce involuntary churn on subscriptions.

Guardrails that protect margins: implement address verification (AVS) and CVV checking to qualify for better interchange on many card-not-present transactions. Use 3-D Secure selectively—enable for high-risk orders or specific geos to shift liability while limiting friction where fraud is already low.

Enable retry logic at smart times (banking hours for ACH, issuer wake windows for cards). For B2B subscriptions, enable Level 2/3 data to lower corporate and purchasing card interchange.

On the back end, choose a gateway with modern APIs, webhooks, and exportable tokens. That keeps you nimble if you later switch acquirers to keep your payment stack affordable. Watch for: gateway surcharges, cross-border acquirer fees, and network token fees—small line items add up over thousands of transactions.

Invoice and B2B Payments: Lower Fees with ACH, Same Day ACH, and Pay-by-Bank

For service firms, agencies, trades, wholesalers, and SaaS with invoices, the most affordable payment solutions for startups and small businesses typically route larger payments off cards and onto bank rails:

- ACH: standard next-day settlement, very low per-item cost.

- Same Day ACH: faster delivery (same-day windows) for time-sensitive invoices. Nacha’s per-payment limit is $1 million, enabling many B2B use cases. Configure cutoffs and notify clients about bank-processing windows.

Build invoice pages that default to pay-by-bank but still offer cards so you don’t lose payers who prefer rewards. If you accept cards, require Level 2/3 data fields in the invoice flow to reduce interchange.

For recurring invoices, add automated reminders, late fees, and partial payments to improve DSO without increasing headcount.

Minimize ACH returns with instant bank account validation (micro-deposits or open-banking checks) and NOC handling. Use SEC codes correctly (WEB, CCD, PPD) and map them to customer consent language in invoices.

The outcome is a blended cost profile that keeps your acceptance flexible while pushing larger-dollar transactions onto lower-cost rails.

Instant Payments: RTP® and FedNow® for Faster Cash Flow

Instant payments have matured from “pilot” to practical tools for affordable payment solutions for startups and small businesses—especially for payouts (contractors, tips, insurance, marketplaces), B2B just-in-time payments, and urgent disbursements.

- RTP® (The Clearing House) runs 24×7 with immediate finality. In 2025, the network increased allowable transaction limits, and reported a major surge in total value processed—evidence that businesses are pushing higher-value use cases onto instant rails.

Ask your bank or payment partner if they support Request for Payment (RfP) for invoice presentment and if they have limits aligned to your ticket size. - FedNow® (Federal Reserve) continues to add participating institutions and build volume. If your primary bank supports FedNow, you can receive (and often send) instant payments, improving cash conversion cycles and reducing the need for expensive same-day wires. Check your provider’s FedNow participation and cutoffs.

Practical playbook: start with instant payouts (to debit cards or bank accounts) for refunds, insurance claims, or marketplace disbursements; then pilot RTP/FedNow for supplier payments under your bank’s limits. Compare fees to wires and couriers; instant rails often win on both speed and cost.

Compliance Essentials (PCI DSS v4.x) Without the Headache

Security and compliance keep payment costs low in the long run by preventing breaches and fines. Under PCI DSS v4.x, fully effective after March 31, 2025, merchants face updated requirements around authentication, customized approaches, password settings, vulnerability scans, and logging.

Work with providers that tokenize card data, support P2PE-validated devices, and scope you down to SAQ A or SAQ A-EP if possible. For ecommerce, avoid touching raw PAN—use hosted fields or iFrames. For staff, enforce MFA for all admin access and segment roles tightly.

If you outsource to platforms (PSPs, gateways), request Attestations of Compliance (AOC) and confirm their v4 readiness.

Bake patch cadence and incident response SLAs into your vendor agreements. Budget now—controls are easier and cheaper to implement during terminal refreshes or checkout redesigns than as bolt-ons later.

Taxes & Reporting: 1099-K Changes Every Founder Should Know

Third-party payment platforms (marketplaces, PSPs, payment apps) issue Form 1099-K to report gross payments for goods and services. For U.S. startups and small businesses using these platforms, tracking rules matters for bookkeeping and to avoid surprises at tax time.

The IRS announced transition relief setting $5,000 as the threshold for calendar year 2024, $2,500 for 2025, and $600 starting in 2026—unless future legislation changes it. Keep records regardless, because 1099-K reports gross, not taxable, income; you’ll still claim deductions for fees, refunds, and returns.

If you operate a marketplace or platform yourself, confirm how your PSP classifies your flows and who issues which 1099 forms.

Fraud, Chargebacks, and Risk: Stop Losses Without Killing Conversion

Fraud isn’t just a security issue—it’s a cost issue. The most affordable payment solutions for startups and small businesses deploy layered defenses that stop attacks while preserving approval rates.

Start with device and IP risk signals, behavioral analytics, velocity rules, and allow/deny lists. Use 3-D Secure (issuer-side authentication) dynamically for flagged transactions. For physical goods, require AVS, CVV, and direct signature for unusually high-value items.

Operationally, track chargeback reason codes and analyze friendly fraud (legit customers filing disputes). Set clear descriptors on statements, send shipping confirmations, and use refund-before-dispute flows when appropriate.

Automate representments with compelling evidence templates (proof of delivery, IP logs, usage logs). Calibrate manual review thresholds to avoid excessive headcount or delays.

For ACH, implement account verification, duplicate checking, and NACHA return code monitoring. For instant payments, build strong payer authentication and leverage RfP to reduce misdirected payments.

Surcharging, Cash Discounting, and Fee Recovery: Proceed Carefully

With slim margins, it’s tempting to offset card fees by surcharging or using cash discount programs. In the U.S., you must implement these programs carefully: rules differ for credit vs. debit, card brand requirements apply, notices and receipt disclosures are specific, and some jurisdictions and card brands impose caps or limits.

Many processors offer compliant programs, but compliance is your responsibility too. Verify that your affordable payment solution for startups and small businesses includes:

- Brand-compliant signage and receipt modifications.

- Proper BIN detection so surcharges never hit debit.

- Accurate settlement accounting so fee recovery posts correctly.

When in doubt, consider dual pricing (visible cash vs. card pricing) or better yet, steer repeat and B2B customers to ACH or instant pay with small incentives—the softer, customer-friendly path to lowering costs without regulatory risk.

Negotiation Tactics: Get a Better Deal from Day One

Even the best provider can be more affordable after you negotiate. Ask for:

- Interchange-plus with a low, flat markup and no monthly minimum during your first months.

- Waived PCI and gateway fees in exchange for a term (but avoid punitive early termination fees).

- Free hardware (or at-cost) on multi-year if devices are modern and not carrier-locked.

- Chargeback support credits and fraud tooling included.

- Annual price-review clause tied to volume growth.

Benchmark with two competing quotes. If you process invoices, request bundled ACH with Same Day windows and instant payouts—packaged pricing often saves more than à-la-carte. Confirm funding times (T+1 or faster) and reserve policies in writing to protect your cash flow.

Build vs. Buy: When to Use a Full-Stack PSP vs. Your Own MID

Early on, a full-stack PSP (aggregated merchant account) is fastest to market and keeps fixed costs low—ideal for MVPs and side hustles.

As you scale, an acquirer + gateway + your own MID often becomes more affordable because you can negotiate markup and gain routing options (e.g., least-cost routing to optimize debit, or multi-acquirer redundancy).

A hybrid approach is common: keep the PSP for low-risk geographies and use a direct acquirer for home-market volume.

Key triggers to revisit architecture: > $1M annual volume, B2B invoices with high ticket, subscription churn tied to card lifecycle events, need for multi-acquirer routing, and platform/marketplace complexity (split payouts, sub-merchant onboarding, 1099-K responsibility). Ensure you retain token portability either way.

Practical Playbooks by Business Type

Retail & Quick-Serve

Aim for EMV + NFC readers with tap-to-pay and integrated POS. Use a unified catalog for online and in-store so inventory, taxes, and discounts stay consistent. Keep costs low with debit optimization and customer-facing wallets.

Add QR pay for line-busting and curbside. Schedule batch settlements to match your deposit preferences, and push larger B2B orders to ACH invoices.

Services & Field Teams

Mobile readers or tap-to-phone cut hardware costs. Send estimates that convert to invoices with pay-by-bank by default and cards/wallets as options. Use on-site card capture for deposits and stored credentials for progress billing.

Adopt Same Day ACH for final invoices where card fees would be high. Configure instant payouts for contractors to improve retention.

B2B & SaaS

Embed Level 2/3 fields in checkout and invoicing. Offer bank pay with instant account verification, and consider RTP/FedNow for just-in-time supplier payments.

Use network tokens and account updater to cut churn, and deploy Smart Retries. For high-ticket, require PO/Invoice matching and enable per-user role controls in your billing portal.

Implementation Checklist (Copy-Paste Ready)

- Scope your channels: in-person, ecommerce, invoicing, payouts.

- Pick pricing: start with interchange-plus quote; collect a flat-rate fallback.

- Add bank rails: ACH + Same Day ACH; pilot RTP/FedNow with your bank.

- Secure it: tokenization, P2PE devices, MFA, and provider AOCs for PCI DSS v4.x.

- Optimize approval: AVS, CVV, selective 3-D Secure, network tokens.

- Tight fraud ops: velocity, device checks, chargeback playbooks.

- Invoice smart: default to pay-by-bank, allow cards, collect Level 2/3.

- Reconcile: daily deposits by tender type; clear descriptors.

- Negotiate: fee waivers, hardware credits, annual price-review clause.

- Review annually: re-price your stack, confirm compliance and 1099-K rules.

FAQs

Q1. What’s the single most cost-saving move I can make this quarter?

Answer: Shift larger invoices and repeat payments to pay-by-bank (ACH/Same Day ACH) while keeping cards/wallets for first-time or small orders. This blend preserves conversion and cuts fees—often your biggest controllable lever for affordable payment solutions for startups and small businesses.

Q2. Are instant payments (RTP/FedNow) worth it for small teams?

Answer: Yes—start with instant payouts (contractors, tips, refunds). The per-payment fee is typically lower than wires and faster than ACH. As banks add features and raise limits, more B2B use cases make sense. Confirm your bank’s participation and limits before committing.

Q3. Do I have to overhaul my systems for PCI DSS v4.x?

Answer: Probably not, if you already use tokenization and hosted fields. But you must ensure MFA, password policies, logging, and assessment scopes align to v4.x. If you’re refreshing terminals or redesigning checkout, bake v4.x into the roadmap now to avoid rework and keep your stack affordable.

Q4. What changed with 1099-K and how does it affect me?

Answer: For TPSO-reported payments, the IRS set transition thresholds of $5,000 (2024), $2,500 (2025), and $600 (2026+). Keep detailed records: 1099-K shows gross payments; your actual taxes consider fees, refunds, and cost of goods. If you are a platform, confirm who issues which forms to sellers.

Q5. Should I surcharge cards to recover fees?

Answer: It can reduce costs but carries compliance complexity. If you try it, use a provider that automates brand rules, signage, debit detection, caps, and reporting. Many merchants instead nudge customers to ACH or offer dual pricing—often a safer, customer-friendly path to an affordable payment solution.

Q6. Flat rate or interchange-plus—what’s better for me?

Answer: For very low volume or early MVPs, flat rate is fine. As you grow, interchange-plus usually becomes more affordable—especially with a strong debit or card-present mix. Ask for both quotes, model your last three months of transactions, and include all fees (gateway, PCI, chargebacks) in your comparison.

Q7. How do I cut chargebacks without adding friction?

Answer: Apply AVS/CVV, clear descriptors, post-purchase confirmations, and a fair refund policy. Use selective 3-D Secure for risky orders only. Automate representment evidence and maintain allow/deny lists. For subscriptions, reduce false declines with network tokens and smart retries.

Q8. When should I move from a PSP to my own merchant account?

Answer: Consider switching when your annual volume tops $1M, average tickets rise, or you need multi-acquirer routing. Owning your MID plus a modern gateway lets you negotiate markups and keep tokens portable—often the path to the most affordable payment solution for small businesses at scale.

Q9. Is tap-to-phone secure enough for card-present acceptance?

Answer: When implemented under current scheme specs and PCI programs, tap-to-phone can be secure and cost-effective for micro-merchants and mobile teams. Confirm your provider’s certifications, device compatibility, and whether offline acceptance is supported within rules.

Q10. What’s the easiest way to start with instant payments?

Answer: Ask your bank or processor about instant payouts to debit or bank accounts; turn it on for refunds, tips, or contractor disbursements. Then pilot RTP/FedNow for supplier payments that benefit from immediate finality. Track costs vs. wires and ACH to keep the program affordable.

Conclusion

The most affordable payment solutions for startups and small businesses don’t hinge on one provider or one rail—they come from mix and match: card-present for impulse and in-person convenience; wallets for mobile conversion; ACH and Same Day ACH for bigger invoices; instant payments for urgent payouts and just-in-time B2B; plus a security posture aligned to PCI DSS v4.x.

Tie it all together with transparent interchange-plus pricing, token portability, and risk controls that protect revenue without blocking good customers.

Treat payments like any other growth channel: measure approval rates, blended fees, dispute losses, and DSO monthly. Re-shop rates annually, and use your data as leverage.

When you make payments affordable, predictable, and fast, you free up cash for inventory, hiring, and product—and that’s how small businesses win in the U.S. in 2025 and beyond.