Running a small business in Pittsburgh—whether you’re slinging pierogies in Polish Hill, repairing bikes in Lawrenceville, pouring lattes in Shadyside, or operating a mobile food truck along the Three Rivers—means every dollar counts.

Card processing is one of those unavoidable costs that can quietly eat into margins if it’s not actively managed. Many owners assume “rates are rates,” and that once you pick a processor the fees are basically fixed.

In reality, merchant services are a complex stack of costs and rules—interchange from the card brands, processor markups, monthly platform fees, PCI and chargeback costs, equipment, and more. The good news is that there are dozens of levers a Pittsburgh small business can pull to reduce total cost without hurting customer experience.

In this in-depth guide, we’ll break down the fee structure in plain English, show you where savings usually hide, and give you a step-by-step action plan you can implement right away.

We’ll also cover neighborhood-specific considerations (like connectivity for mobile vendors at events), seasonal tactics for tourism surges (e.g., game days and festivals), and best practices for restaurants, retail, service trades, and B2B merchants.

By the end, you’ll understand what you’re paying for, how to benchmark it, which changes deliver the biggest ROI, and how to renegotiate your pricing with confidence—so you can keep more of every sale and reinvest in what matters: your customers, your team, and your growth.

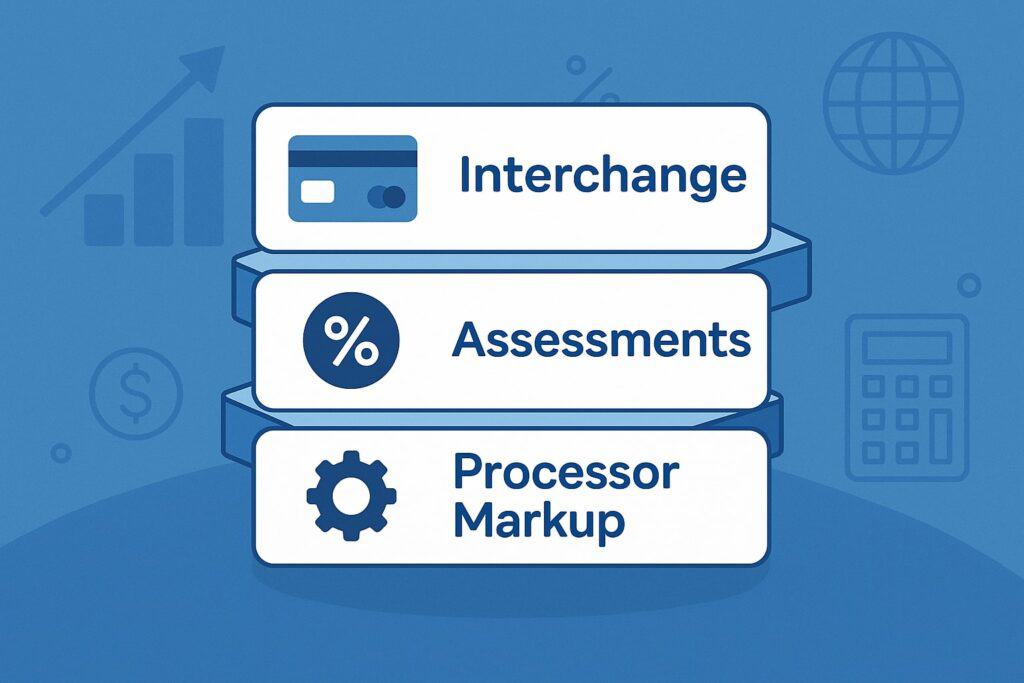

Understand the Fee Stack: Interchange, Assessments, and Processor Markup

The first step to saving money on merchant services is understanding where the money goes. Every card transaction triggers three layers of cost. First is interchange, which is the wholesale fee paid to the issuing bank (the bank that gave your customer their card).

Interchange is non-negotiable on a per-merchant basis and varies based on card type (debit vs. credit; rewards vs. non-rewards), entry method (chip/PIN, contactless, keyed), business category (MCC), and transaction details (ticket size, presence of AVS/ZIP, tip formatting, etc.).

Second are card brand assessments, small network fees charged by Visa, Mastercard, Discover, and American Express. Like interchange, assessments are not something your processor can change for you. Finally, there’s processor markup—the negotiable piece you can (and should) optimize.

Markup includes the rate plan (e.g., interchange-plus vs. tiered vs. flat), gateway or POS software fees, monthly account fees, PCI-related fees, chargeback handling, statement fees, and equipment or SaaS subscriptions.

If you look at your statement and see only a single “flat” number, it can feel simpler, but that simplicity often hides higher total cost. Interchange-plus tends to be the most transparent and often the most economical at scale, because you’re paying true interchange plus a clear, competitive markup.

Tiered pricing can group transactions into “qualified,” “mid-qualified,” and “non-qualified,” but those buckets are opaque and can push many of your transactions into more expensive tiers.

The key is being able to map any quoted rate plan back to the same baseline: total effective rate (total processing cost divided by gross card volume). When you analyze the full stack with this lens, you can compare apples to apples and see exactly which levers drive your all-in cost down.

Audit Your Statement Like a Pro: Where Pittsburgh Businesses Typically Overpay

Once you understand the fee stack, the next step is a systematic statement audit. Pull at least three months of recent statements (include a busy month if your business is seasonal). Calculate your effective rate: total fees ÷ total card sales.

For many small businesses, a healthy benchmark is often somewhere in the 2%–3% range for a blended mix of debit and credit—though your specific mix (average ticket, card present vs. online, tips, rewards card prevalence) can shift that baseline up or down.

Next, isolate processor markup by subtracting posted interchange and assessment totals (if shown) from your total cost. If your statement doesn’t itemize interchange and assessments, request an interchange-plus quote and a sample cost comparison.

Common red flags:

(1) Non-itemized “non-qualified” surcharges that seem to hit a large share of your transactions;

(2) Monthly junk fees like “regulatory fee,” “network access fee,” or “PCI non-compliance” fees that persist even after you’ve completed your PCI SAQ;

(3) Gateway fees stacked on top of POS subscriptions;

(4) Batch fees charged daily that add up;

(5) Excessive chargeback fees that may be mitigated with better descriptor, AVS/CVV rules, or pre-dispute tools; and

(6) Lease payments on terminals that far exceed the device’s purchase price.

Pay attention to debit routing: many statements do not clearly show whether regulated debit (from large banks) is taking the least-cost route via network choice, and unregulated debit might be defaulting to the most expensive path.

Restaurants should examine how tips are handled (e.g., whether the processor applies a higher rate for tipped transactions or for “adjusted” tips after authorization).

E-commerce sellers should verify whether keyed-in orders are priced higher than chip or tap sales, and whether address verification (AVS) is being applied consistently to help qualify for better interchange categories.

Finally, capture the chargeback ratio by volume and count, note the reason codes, and identify patterns (e.g., recurring disputes after online orders ship). Disputes can be costly beyond fees—lost goods, labor time, and potential penalties—so tightening dispute prevention often pays dividends quickly.

Choose the Right Pricing Model and Negotiate Markup—Without Hurting Customer Experience

With a clean picture of your current costs, choose a pricing model that fits your sales pattern and your comfort with variability. Interchange-plus is usually the best fit for merchants whose volume is growing, whose mix includes both debit and credit, and who value transparency.

You’ll see true interchange pass-through plus a small, fixed markup (e.g., 0.15% + 8¢). As your mix improves (more regulated debit, more chip/tap transactions), your total effective rate can drop.

Flat-rate plans can be fine for micro-merchants or very low volume because of their predictability, but watch out for premium pricing on debit, chargebacks, and keyed transactions.

Tiered plans are rarely the cheapest, but some POS providers push them; if you’re on tiered today, ask for an interchange-plus quote using your past three months of data for a direct comparison.

When negotiating markup, come prepared: show your effective rate and what parts you believe are negotiable (per-transaction fees, monthly account fees, gateway fees, and PCI-related fees).

Ask for fee waivers on line items that do not add value (e.g., “regulatory fee,” “POS non-integrated surcharge”) and for volume-based discounts as you grow. If you operate across multiple locations—from the Strip District to Mount Washington—see if you can aggregate volume for better pricing while still receiving location-level reporting.

Keep customer experience front and center: the goal is lowering cost without adding friction. For example, enabling PIN debit or contactless wallet acceptance can lower cost and speed up checkout.

If your processor suggests heavy-handed tactics (like forcing 100% keyed CVV entry in-store), discuss the likely impact on speed and customer satisfaction before you agree. Good savings strategies should be invisible to the shopper but visible on your P&L.

Optimize Transaction Quality: The Checkout Settings That Lower Interchange

Beyond your processor’s markup, you can qualify for better interchange by improving transaction quality. For card-present sales, make sure you’re chip-first and contactless-enabled.

EMV chip or NFC transactions typically carry lower risk and better interchange than swiped or keyed-in entries. If your POS allows it, prefer PIN debit for eligible debit cards: it often routes through lower-cost debit networks.

Confirm your terminal supports least-cost routing for debit and that the feature is enabled correctly. For keyed or online transactions, enforce AVS (Address Verification Service) and CVV collection; some interchange categories require AVS for the best pricing, and CVV helps both risk scoring and dispute defense.

If you invoice B2B customers, enable Level II and Level III data—things like tax amount, customer code, and line-item details—which can drop interchange on corporate and purchasing cards.

Restaurants can reduce expensive downgrades by closing batches daily at a consistent time, properly handling tip adjustments (complete them within the allowed window), and ensuring transactions are settled promptly after authorization.

For recurring billing (gyms, salons, services), use tokenization and account updater tools to keep cards current and reduce declines; fewer retries means fewer extra authorizations that can raise costs or trigger fees.

Small improvements compound: shaving 5–10 basis points by qualifying better interchange plus 5–10 basis points on debit routing plus 5–10 basis points on negotiated markup can add up to hundreds or thousands of dollars saved per month for many Pittsburgh merchants.

Make these settings part of your standard operating procedures—once configured, they quietly work in the background every day.

Debit Routing, Surcharging, and Dual Pricing: What’s Possible and What to Watch

Three of the most talked-about cost strategies today are debit routing, surcharging, and dual pricing/cash discounting. Debit routing (also called network choice) lets your system pick among debit networks for the least-cost route.

To benefit, your hardware and processor must support it, and your cashier workflow should encourage PIN when appropriate (without slowing the line). The savings can be significant for merchants with a high share of debit transactions, such as convenience/quick-serve and small retail.

Surcharging—adding a fee to credit card transactions—can offset processing costs, but it comes with card brand rules, signage requirements, and caps. It also carries customer-experience tradeoffs: some shoppers will react negatively, and you must never surcharge debit.

Because compliance rules, card-brand requirements, and local expectations can change, treat surcharging as a carefully planned program: test it, measure impact on conversion and satisfaction, and ensure your software calculates it correctly and itemizes it on receipts.

Dual pricing (also called cash discounting or “price at register” programs) offers a lower cash price and a standard price for cards; when executed correctly, this can be simpler for staff and customers and may avoid some surcharge complexity, but it still requires strict receipt and signage clarity.

For both surcharging and dual pricing, check applicable rules and ensure your implementation matches what your POS and gateway support; your goal is to reduce cost without creating disputes, negative reviews, or compliance issues. Pittsburgh’s neighborhood vibe—where many shops rely on repeat customers—means your pricing presentation matters.

If you try a program, communicate the “why” (rising card costs, small margins), thank customers for supporting local business, and give wallet-friendly alternatives like contactless debit or cash.

Hardware, Software, and Connectivity: Keep It Simple, Fast, and Cost-Aware

Your POS stack can either compound fees or control them. Start with the acceptance channels you actually need: counter, tableside, handhelds for curbside, online ordering, invoices, and recurring billing.

Many all-in-one POS suites bundle features you won’t use, so pick a plan that matches your operation. Avoid long-term terminal leases; in most cases, buying devices outright is cheaper than leasing.

Confirm your terminals are EMV and NFC capable and support tip prompts (for restaurants), PIN debit, and offline mode for brief connectivity dips at festivals, pop-ups, or farmer’s markets.

For mobile sellers at events like Picklesburgh or Three Rivers Arts Festival, plan for redundant connectivity (dual SIM hotspots or carrier diversity) so you’re not forced into offline fallbacks that may raise risk and, in some setups, cost.

On the software side, scrutinize gateway fees if you’re already paying for a POS subscription—sometimes you’re double-paying for routing.

If you take invoices or online orders, ensure your checkout flow is streamlined: fewer fields, auto-fill address, AVS and CVV enabled, clear tax and delivery fees, and a recognizable statement descriptor (including your city, e.g., “ABC Bakery PITTSBURGH PA”) to prevent “I don’t recognize this” disputes.

Consider tap-to-pay on iPhone or Android for pop-up or overflow lanes to reduce hardware costs and speed lines on game days. For restaurants, tableside pay minimizes card handoffs, speeds turns, and can cut walk-outs; for retail, scan-and-go or “line busting” with handhelds can increase throughput during holiday markets.

Keep devices updated, change default passwords, and follow PCI Self-Assessment annually to avoid non-compliance fees. Simpler, modern hardware plus clean software configuration doesn’t just save pennies—it protects your brand experience while shaving meaningful basis points across thousands of transactions.

Reduce Chargebacks and Fraud: Prevention Beats Recovery Every Time

Chargebacks cost much more than the listed fee. There’s lost inventory or service time, administrative labor, possible chargeback monitoring thresholds, and the morale hit when your staff deals with disputes.

Start by improving descriptor clarity: include your business name customers recognize and “Pittsburgh, PA” or your neighborhood; mismatched names are a top trigger for “fraud” claims.

For card-present sales, use EMV/NFC, capture signatures only when your vertical still requires it (most don’t for liability), and consider PIN prompts for higher-ticket transactions.

Train cashiers to verify ID only when appropriate and to spot common red flags (split payments across multiple cards, rushed buyers, or requests to ship to alternate addresses). For e-commerce and invoice payments, enable AVS, CVV, and consider 3-D Secure or step-up authentication for risky orders.

Use velocity checks (e.g., no more than X attempts per card or IP in Y minutes) and maintain deny lists of email/phone/IP for confirmed fraud. Provide clear refund/return policies on receipts and your website, honor promised timelines, and document delivery or service completion (photos, signed work orders).

Respond to disputes quickly with organized evidence: receipt, delivery confirmation, tip adjustments, customer correspondence, and policy disclosures. If you’re selling tickets or services near major events (Steelers, Penguins, Pirates games), expect higher fraud attempts and tighten settings temporarily.

Over time, merchants who invest in layered prevention see fewer disputes, lower fees, and stronger standing with their processors—often unlocking better pricing because your risk profile improves.

Tactics by Vertical: Restaurants, Retail, Services/Trades, and B2B

While the fundamentals apply to everyone, each vertical in Pittsburgh has unique levers for savings. Restaurants should ensure proper tip-adjust workflows (close batches daily, limit manual edits), use quick-tip buttons to speed checkout, and consider order-at-table or counter-pickup flows to reduce staff handoffs.

Explore dual pricing with crystal-clear menu labeling if you choose to offset card costs, and make sure online ordering uses stored tokens for repeat customers to reduce declines.

Retail can lean into contactless and PIN debit, deploy handhelds for peak weekends, and keep SKU-level data clean for inventory and fraud analytics. Consider return policies that minimize abuse without friction (e.g., digital receipts tied to card tokens).

Service and trades (contractors, home repair, mobile detailers) should prioritize on-site chip/tap acceptance instead of taking cards over the phone, use e-invoices with AVS/CVV and optional bank-to-bank payment links, and set deposit/authorization holds correctly to avoid downgrades.

B2B merchants should turn on Level II/III data, consider ACH and RTP for large invoices (with small convenience fees when appropriate), and negotiate surcharging or dual pricing carefully with contract language that mirrors card-brand rules.

Across all verticals, use data exports to track effective rate weekly or monthly and study correlations: average ticket vs. cost, debit share vs. cost, and processor markup vs. volume. That visibility turns fee control into an ongoing habit rather than a once-a-year task.

How to Renegotiate Your Contract (and When to Switch)

If your audit reveals excessive markup or rigid fees, it may be time to renegotiate. Gather three months of statements, summarize your effective rate, list pain points (fees, support responsiveness, feature gaps), and request an interchange-plus quote with a simple markup (basis points + per-transaction).

Ask for month-to-month terms or short commitments with caps on fee increases. If you’re on a lease, calculate the buyout vs. purchasing new hardware; long leases can quietly eat thousands of dollars.

Press for PCI fee waivers when you maintain compliance, and ensure gateway fees are not duplicated by your POS plan. If your current provider cannot meet reasonable targets—or if support has been poor—plan a switch with minimal downtime: parallel test on a new terminal, migrate tokens for recurring customers, and switch batches mid-week during slower hours.

Train staff on the new prompts (tips, PIN, receipt options) and post temporary signage so customers know you’re upgrading systems. After the switch, monitor the first two statements to ensure the promised pricing is live and that debit routing and Level II/III settings are working.

The best test of a good deal is not just a sharp headline rate but clean, stable statements and a support team that helps you chase down basis-point wins over time.

Seasonal and Local Considerations for Pittsburgh Merchants

Pittsburgh’s calendar has a rhythm: sports seasons, university move-ins and graduations, summer festivals, holiday markets, and weather swings. Use that cadence to lower merchant costs and protect revenue.

Ahead of big weekends (Steelers home games, marathon weekend, arts festivals), enable additional handhelds or tap-to-pay lanes so you can push more traffic through lower-cost, card-present transactions instead of backing up and keying cards.

For outdoor events where connectivity is unreliable, prep two carriers or a hotspot and test terminals in advance; offline fallback modes can be lifesavers but may carry higher risk or result in higher downgrade rates if batches settle late.

In winter, when in-store traffic dips and online orders rise, tune AVS/CVV rules and consider 3-D Secure as needed. For neighborhoods with a high share of student customers, expect more debit (good for cost) but also educate staff on receipt clarity to prevent disputes from unfamiliar descriptors.

If you do pop-ups at Strip District or farmer’s markets, choose lightweight hardware and fixed-fee add-ons carefully; paying an extra monthly for features you only use three weekends a year rarely pencils out.

Pittsburgh’s local-first pride also means that customers often respond well when you explain (tactfully) how card costs affect small businesses; if you implement dual pricing, a friendly one-liner on signage can preserve goodwill while achieving savings.

A Step-by-Step 30-Day Plan to Lower Your Fees

- Day 1–3: Gather three months of statements and compute effective rate plus a line-item list of monthly and per-transaction fees.

- Day 4–7: Confirm POS settings—chip/tap first, PIN debit enabled, debit routing on, AVS/CVV for online/keyed, daily batch close, and tip adjust workflow.

- Day 8–10: Turn on Level II/III for B2B cards and test an invoice with expanded fields. Day 11–14: Call your processor to request interchange-plus with a clear markup, removal of non-value monthly fees, and PCI fee waiver if compliant.

- Day 15–18: Implement descriptor improvements, post any signage for pricing programs, and train staff on PIN prompts and exception handling.

- Day 19–22: Review chargeback data, tighten rules (velocity limits, 3-D Secure for risky orders), and publish/refine your refund policy.

- Day 23–26: Evaluate hardware (avoid leases), add tap-to-pay for mobile lanes, and ensure redundant connectivity for events.

- Day 27–30: Recalculate effective rate on the latest batch and project annual savings. Keep a simple dashboard: total volume, debit share, average ticket, chargebacks, and effective cost.

Repeat quarterly. This cadence, more than any single trick, is what keeps savings locked in despite changing card mixes and network adjustments.

FAQs

Q.1: How do I know if my effective rate is actually good for my type of Pittsburgh business?

Answer: The best way to judge your rate is to compare your all-in effective cost to your peers’ operating realities—average ticket size, share of debit vs. credit, and how you accept cards (in-person, online, or keyed).

A coffee shop with a $7 average ticket will see proportionally higher per-transaction cost share than a fine-dining restaurant with a $60 average ticket, even if both have the same markup, because the fixed per-transaction fee (the “¢” part) makes up a bigger slice.

Similarly, stores with a high fraction of regulated debit (common among younger customers and students) can achieve lower effective rates than shops whose clientele skews toward rewards credit.

A good baseline test is to grab three months of statements, compute total fees ÷ total volume, and then adjust expectations based on your mix. If you’re consistently above your vertical’s typical range—say, materially higher than 3% for a mostly in-person retailer—start auditing markup line items and transaction qualification settings.

Often, simply enabling PIN debit, daily batch close, and AVS/CVV where appropriate can shave meaningful basis points before you even renegotiate.

And remember: “simple flat rate” doesn’t equal “cheap”—transparency beats simplicity when you’re large enough for pennies to matter, which is true for many Pittsburgh merchants once they pass a few thousand dollars a month in card sales.

A second lens is to measure trends rather than snapshots. Your effective rate will fluctuate with seasonality, promotional events, and card mix. What matters is whether your 12-week moving average is drifting up (a red flag signaling downgrades, new fees, or card mix shifts) or down (indicating successful optimization).

Keep a one-page tracker with five fields—volume, average ticket, debit share, chargebacks, and effective rate—and update it monthly. If you implement a change (e.g., level-III data, dual pricing, new gateway), annotate the date and look for impact over the next two statement cycles.

This approach gives you confidence that your rate is not just “good today” but staying good, even as networks tweak rules and your business mix evolves through football season, festivals, and the holidays.

Is surcharging or dual pricing right for my shop, and will customers push back?

Surcharging and dual pricing can offset card costs, but the right choice depends on your brand, neighborhood, and customer expectations.

In tight-knit areas like Bloomfield or Squirrel Hill, regulars value relationships—so if you surcharge, be transparent and polite about why. Make sure your POS supports automatic, compliant calculation and that staff can explain the policy briefly without debate.

Never surcharge debit; that’s a card-brand no-go. Dual pricing (clearly labeled cash price vs. card price) can feel more natural for some merchants and avoids adding a separate “fee” line that irks customers, but it still requires proper receipt/itemization and signage.

The safest route is to pilot at one location or for specific lanes, measure any change in conversion and average ticket, and read feedback. If you see significant pushback or lower tips in restaurants, reconsider the structure or consider PIN debit encouragement and other behind-the-scenes strategies first.

From a financial standpoint, model the elasticity of your customers. If your average margin is thin and card costs approach 3%–3.5%, a modest card price differential may preserve your margin without reducing traffic.

But if your competitive set includes big-box stores that absorb fees silently, a surcharge could feel out of step and risk churn.

Remember that Pittsburgh consumers also use mobile wallets and debit frequently; optimizing for least-cost debit routing, contactless speed, and Level II/III data for B2B might yield most of the savings you need without changing the customer-facing price at all.

Ultimately, aim for the solution that reduces cost and preserves loyalty—because long-term goodwill is worth far more than a few basis points.

Q.2: What’s the fastest way to cut 20–50 basis points off my costs without switching providers?

Answer: Start with settings, not contracts. Turn on PIN debit and least-cost routing for eligible cards; enable chip/tap first; enforce AVS/CVV for keyed/online orders; set daily batch close; and confirm Level II/III for B2B.

These changes alone often carve out 10–30 bps. Next, review your statement for avoidable monthly fees—PCI non-compliance (complete your SAQ), duplicate gateway fees, and extraneous “regulatory” or “statement” fees.

Ask your provider to waive or credit them going forward. Then, fix your descriptor and refund policy clarity to reduce friendly fraud and chargebacks.

Finally, if you’re leasing terminals, run the math on buying hardware outright; the savings over 12–24 months can translate to another 5–10 bps on your effective rate at typical volumes. You can implement this entire checklist in under a month and see the impact by your next statement cycle.

If you still need more relief, consider a micro-pilot of dual pricing at one register or for certain product lines with clear signage and staff training. Keep the pilot short (two to four weeks), compare conversion, average ticket, and customer sentiment, and make a data-driven decision about broader rollout.

This structured approach minimizes risk while giving you a clear path to the 20–50 bps reduction you’re targeting—often without the operational headache of a processor switch.

Conclusion

For Pittsburgh small businesses, merchant services don’t have to be a black box or a constant drag on margins. With a clear understanding of the fee stack, disciplined statement audits, a transparent pricing model, and a handful of high-impact configuration changes, you can push your effective rate meaningfully lower—while actually improving checkout speed and customer experience.

The biggest wins come from smart routing of debit, clean EMV/NFC execution, Level II/III for B2B, tight dispute prevention, and firm but fair markup negotiations with your provider.

Layer in neighborhood-smart operations—mobile connectivity for events, staff training for peak days, and hardware that fits your footprint—and you’ll lock in savings that compound month after month. Remember: this isn’t a one-time project.

Make fee control a quarterly habit, track a few simple metrics, and keep your POS and policies aligned with how Pittsburghites really shop, dine, and pay.

Do that, and your merchant services will stop being an expense you endure and become a performance lever you control—freeing up cash to invest in better products, better people, and the next stage of your growth.